Investors Bullish on Development Asset Opportunities in India, Investments Surge Seven-fold in 2018 Year to date $960 Mn

The last decade or so has witnessed the risk appetite of foreign and domestic investors changing across different asset classes in India’s realty sector. Pivotal events like the Lehman Brothers collapse and the subsequent global financial meltdown were major triggers behind the increased risk perception.

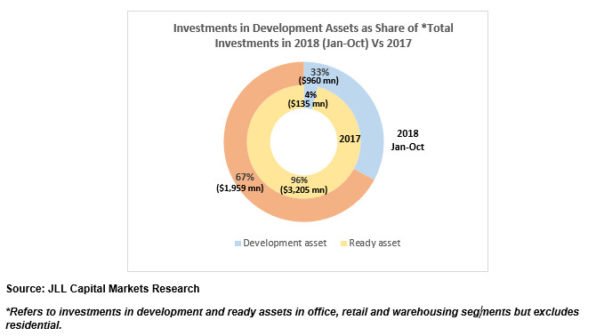

- Investments in development assets as share of total investments across various real estate asset classes (excluding residential) have risen to 33% in current year till date from 4% in 2017

The last decade or so has witnessed the risk appetite of foreign and domestic investors changing across different asset classes in India’s realty sector. Pivotal events like the Lehman Brothers collapse and the subsequent global financial meltdown were major triggers behind the increased risk perception. However, transformative regulatory reforms such as GST, demonetisation and RERA along with focus on affordable housing, easing of FDI norms in construction sector, and infrastructure status to affordable housing and warehousing segments has seen investors’ confidence returning back in the domestic realty sector.

This confidence reflects in the total value of institutional investments in the real estate sector since 2014. Investments have nearly tripled to $6.4 billion in 2017 from $2.2 billion in 2014. Maintaining that momentum, the first half of 2018 has already witnessed robust numbers with $3.6 billion of investments.

While the investment figures are an important indicator of institutional investors betting big on the Indian realty sector, a major trend emerging in the last few years is of investors putting money in development assets. Development assets includes realty projects that are either in under construction phase or undergoing restructuring, as well as greenfield. However, these do not include residential projects.

According to JLL data, investments in development assets have increased to $960 million in the current year till date from $135 million in 2017. In percentage terms, investments in development assets as share of total investments across various real estate asset classes (excluding residential) has seen an eight fold jump to 33% in 2018 year-to-date compared to 4% in 2017.

So what are the key factors behind investors fancy for development assets?

Favourable macroeconomic indicators: Indian economy grew by an impressive 8.2% in first quarter of 2018-19, extending the sequential acceleration to four successive quarters. While industrial growth maintained a robust pace in June-July 2018 on a year-on-year (y-o-y) basis, the IIP numbers were a bit muted for August. Also, the retail inflation data in September remaining within the Central Bank’s medium term target of 4% and government’s intent to keep fiscal deficit at 3.3 % of GDP for 2018-19 augur well for the economy.

Regulatory reforms in real estate leading to more transparency: Implementation of reforms like Real Estate (Regulation and Development) Act, Goods and Services Tax Act (GST) and Benami Transactions (Prohibition) Act have contributed to increasing transparency in real estate sector leading to improved investor confidence. The increased transparency is reflected in India moving to 35th spot in JLL’s Global Real Estate Transparency Index 2018 from the 40th spot in 2014.

Within development assets, office, retail and warehousing segments have attracted institutional investments.

Office markets have been the preferred destination for institutional investors. Opportunistic foreign funds were first to spot the potential in this space. They bought large office assets with attractive yields in view of future public exit via REITs. For instance Blackstone along with its joint ventures with Embassy Group, Salarpuria Sattva, Panchshil Realty and K Raheja Corp. owns 78 mln sq ft. while Brookfield has built an office space portfolio of 24 mln sq. ft These investors have acquired 100-120 mn sq ft of quality stock which has led to limited availability of ready grade A office assets for investments. This coupled with increased transparency of the real estate sector makes a case for higher investments in ‘development assets’ in coming years.

Well established malls have been an attractive destination for investors looking to invest in Indian retail segment. For instance, GIC bought 50% stake in Viviana Mall, Thane while Blackstone acquired stake in Forum Group’s Esplanade Mall in Bhubaneswar. However, limited availability of well operated malls have turned the focus of investors towards development assets. As a result, investment platform funds/joint ventures have been the preferred model of investments in the retail segment. The global experience and patient capital from large institutional funds at development stage is expected to invigorate the retail sector with global best practices and provide long term horizons.

- Virtuous Retail South Asia Pte. Ltd. (A Xander Group Inc. and Dutch pension fund APG-JV) – 2018

- Island Star Mall Developers (CPPIB and Phoenix Mills JV) – 2017

- Nexus Mall Ltd.(Blackstone subsidiary) – 2016

Another segment with significant development assets potential is warehousing sector. Historically, warehousing has been predominantly an unorganized segment and has witnessed limited deals by global investors. For instance, Canada Pension Plan Investment Board (CPPIB) and IndoSpace Ltd. have formed a joint venture named IndoSpace Core to acquire and develop modern logistics facilities in India. The landmark GST reform is expected to bring consolidation and drive emergence of large technologically advanced warehouses in certain sectors like FMCG, e-tailing and manufacturing sector.

The warehousing demand is also expected to get further boost from the “Make in India” initiative and various industrial corridors under progress. Significant growth in retail sector including e-tailing is expected to drive further demand for modern warehousing facilities. The focus on technology is evident from the recent announcement of long term strategic tie-up between industrial real estate company IndoSpace and modern logistics and technology-led solutions provider GLP.

Developers with long-term vision, focus on corporate governance principles, and ability to forge strategic partnerships will be the ones to benefit from increasing interest in ‘development assets’. Rising investor confidence, solid appetite of global investors and inclination of marquee developers for joint venture is likely to usher in more ‘development asset’ investments moving ahead.

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. Our vision is to reimagine the world of real estate, creating rewarding opportunities and amazing spaces where people can achieve their ambitions. In doing so, we will build a better tomorrow for our clients, our people and our communities. JLL is a Fortune 500 company with operations in over 80 countries and a global workforce of 88,000 as of September 30, 2018. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.com