Over 7-fold rise in capital raised by Real Estate investment platform Funds /JVs in last six years

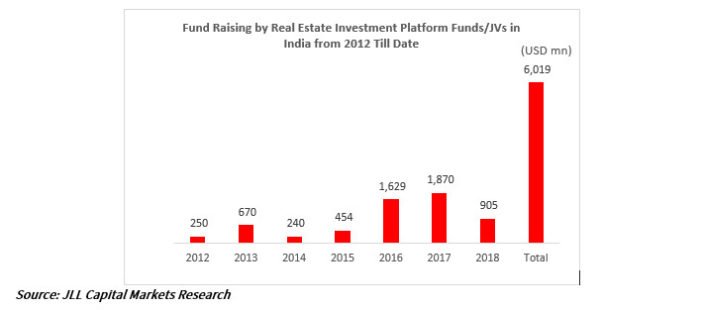

In India, the trend of dedicated investment platform funds/JVs started with the tie up of Godrej Properties and Dutch asset management firm APJ for their real estate investment platform fund in 2012. Till date, these India-focused platform funds have received total commitment of $6.0 bn.

- On a cumulative basis, these funds have raised $6 billion since 2012 till date

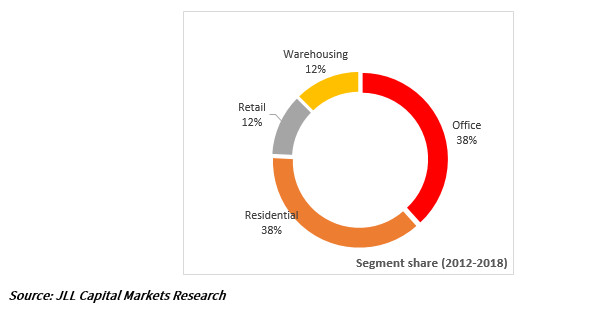

- 38% of capital raised by these funds committed to commercial office space due to huge opportunities

- Affordable housing and retail – the new mantra for funds

- Warehousing and industrial assets to drive future platform deals

Post the global financial crisis, funds with minimal participation from investors haven’t quite performed well. This has provided an opportunity for emergence of real estate investment platform funds /JVs with investors playing an important role in decision making.

In India, the trend of dedicated investment platform funds/JVs started with the tie up of Godrej Properties and Dutch asset management firm APJ for their real estate investment platform fund in 2012. Till date, these India-focused platform funds have received total commitment of $6.0 bn.

Though blind pool funds (with unstated investment goals) still account for a major chunk of the capital raised, Indian real estate focused platform/JVs have witnessed a seven-fold jump to nearly $1.9 billion in 2017 from $ 250 million in 2012. This significant rise in fund raising has been driven by investors seeking more direct control over their investments. Focused strategy and objectives have been key to facilitating deal evaluation and faster decision making.

These platforms aim at building long-term partnership with developers across various real estate asset classes. The rising investor confidence is being reflected in the form of equity investments in projects which is helping JV/platform deal model pick up pace. For the sector and end-users, the partnership of large funds and good pedigree developers has been quite beneficial.

In terms of absolute numbers, these funds have raised $6 billion till date from 2012. Of this, $905 million has been raised in the current year till date.

Some recent key examples of real estate investment platform funds/JVs are given below:

- Qatar Investment Authority-RMZ Corp raised $300 mln in 2013

- Standard Chartered – Tata Realty and Infrastructure committed $450 mn in 2016

- APG Asset Management N.V. – Godrej Fund Management raised capital worth $450 mn for Godrej Build to Core-I Fund in 2018

Investments in brownfield/ build to core developments are key destination for platform level tie-ups between established commercial developers and global PE players. Investment strategies are being fine-tuned for more development risk to ensure higher portfolio returns. Developers in India are increasingly willing to form joint ventures with foreign investors due to tighter lending norms by domestic banks.

In terms of the share of various real estate asset classes in the total capital raising by investment platform funds during 2012-18, grade-A office and residential segments have 38% share each respectively.

Within the overall residential space, affordable housing has 71% share of the total financing committed by these platform funds totalling to $1.6 bn raised. Some recent key transactions in the affordable segment includes Prestige Estate Project Ltd. and HDFC Capital Advisors together committing Rs 2.5 billion. Puravankara Developers is also in talks with domestic investment funds for their affordable housing projects. Affordable housing is also expected to see greater interest with incentives offered by the government are likely to result in better end-user and developer participation.

Among other asset classes, the retail segment also has been witnessing the momentum with a share of about 12% in funding raised, signalling growing investor confidence in this sector. Phoenix Mills Ltd. and CPPIB forming investment platform of around $250 million in 2016 and APG-Xander Group co-investing $450 million in 2017 are some major examples in the retail segment. Besides investing in operating malls, these funds have acquired greenfield projects as well, thus taking up the role of a developer. Apart from providing growth capital, these platforms will also bring in global expertise and best practices in retail assets. The retail sector is likely to find investors for core assets in smaller urban centres, while platform structures will also gain prominence with players who have managed to show sustained performance.

Industrial and warehousing segment, which has a share of 12% of the total capital raising by investment platform funds, is expected to witness paradigm shift with new industry 4.0 revolution and landmark changes introduced by GST. Post GST, we are witnessing consolidation and emergence of large warehouses in certain sectors. This will provide a conducive environment for technology to flourish. Robotics, Internet of Things and artificial intelligence will bring paradigm shift with efficiencies and economies of scale. Government’s focus on ‘Make in India’ and industrial corridors is expected to drive increased demand for warehousing space. Large funds with patient capital have an opportunity for superior risk adjusted returns from this segment. This asset class is expected to be the emerging major theme for investors.

Investment platform funds are a clear signal of the coming of age of Indian private equity players and the maturity. The market share of these funds is rising despite blind pool funds being the mainstay. These funds are fuelling growth of various asset classes like residential, office and retail in larger volume by providing patient capital to competent developers. However, we feel that industrial and warehousing segment as an emerging asset class is expected to witness more platform deals in near term in the backdrop of landmark regulatory changes.

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. Our vision is to reimagine the world of real estate, creating rewarding opportunities and amazing spaces where people can achieve their ambitions. In doing so, we will build a better tomorrow for our clients, our people and our communities. JLL is a Fortune 500 company with operations in over 80 countries and a global workforce of 88,000 as of September 30, 2018. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.com